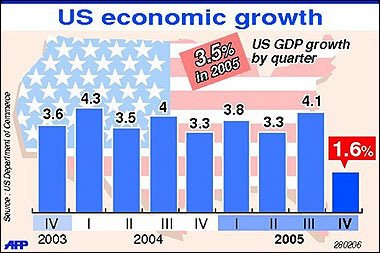

Graphic of US economic growth rate as the fourth quarter 2005 is revised upwards from 1.1 % to 1.6 %.(AFP)

Graphic of US economic growth rate as the fourth quarter 2005 is revised upwards from 1.1 % to 1.6 %.(AFP)Here's a couple economic stories that I found off Yahoo News. I'm not sure how to comment on them. The first story is titled, Job Fears Push Down Consumer Confidence:

NEW YORK - Americans in February became less optimistic about the overall economy, especially the short-term prospects for the job market, sending a widely followed barometer of consumer sentiment below analysts' estimates.

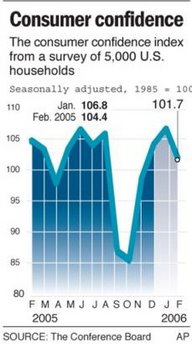

The Conference Board, a New York-based private research group, said Tuesday its consumer confidence index fell to 101.7, from a revised 106.8 in January, the highest level since May 2002. The drop in February stalled a rebound in the index that began in November following the Gulf Coast hurricanes. Analysts had expected a reading of 104.0 in February.Chart shows consumer confidence for the past 13 months. (AP Graphic)

In a statement, Lynn Franco, director of The Conference Board Consumer Research Center, said "consumers are growing increasingly concerned about the short-term health of the economy and, in turn, about job prospects."

But consumers' assessment of present conditions is holding steady at a four-and-a-half-year high, suggesting that the start of 2006 will be better than the end of 2005, Franco said.

The report came as the Commerce Department reported that the economy grew at an annual rate of 1.6 percent in the final quarter of 2005, a lackluster performance but still slightly better than originally thought.

Stock prices fell as traders worried the stronger-than-expected growth in gross domestic product could prompt the Federal Reserve to continue raising short-term interest rates. In afternoon trading, the Dow Jones industrial average fell 99.17, or 0.89 percent, to 10,998.38.

The Standard & Poor's 500 index fell 12.72, or 0.98 percent, to 1,281.40.

The component of the consumer confidence index that assesses views of current economic conditions rose to 129.3 from 128.8. But another component that measures consumers' outlook over the next six months, the Expectations Index, fell to 83.3 from 92.1 in January.

Excluding the two months following Hurricane Katrina, the Expectations Index in February was at its lowest level since March 2003, when it was 61.4. Franco warned that if expectations continue to lose ground, the outlook for the remainder of the year could deteriorate.

Now here's the second story that I found off Yahoo News. This one is titled, Economy Grows at Mediocre Pace:

WASHINGTON - The economy, sagging under the strain of lofty energy prices, grew at an annual rate of 1.6 percent in the final quarter of last year — a mediocre performance that nonetheless turned out to be slightly better than first thought.Chart shows quarterly rate of change in the gross domestic product. (AP Graphic)

The new reading on gross domestic product, released by the Commerce Department on Tuesday, did represent an upgrade from the 1.1 percent growth rate initially estimated for the October-to-December quarter. Still, economic growth under the new GDP figure — as well as the old one — was the slowest in three years and clearly showed a loss of momentum from the third quarter's brisk 4.1 percent pace.

Economists, however, said the economy is already rebounding smartly from the end-of-year lull. They predict growth will clock in at a robust 4.5 percent pace in the current January-to-March quarter.

Gross domestic product measures the value of all goods and services produced within the United States and is considered the best gauge of the economy's performance.

The fourth quarter's slowdown was blamed on the lingering fallout of the Gulf Coast hurricanes and elevated energy prices, which caused consumers especially to tighten their belts. Analysts said the final quarter's performance was more like the economy hitting a pot hole on the road of expansion, rather than a sign of a more serious derailment.

Indeed, other recent economic barometers — including production, retail sales and jobs — suggested the economy did start bouncing back at the beginning of this year. The nation's unemployment rate dropped to 4.7 percent in January, the lowest in 4 1/2 years.

Now here's a third Yahoo News story--this one about housing. This story is titled, Housing market cools, pace of resales slows:

WASHINGTON (Reuters) - The U.S. housing market has begun to cool, new data showed on Tuesday, as the pace of home resales slowed in January and the number of homes on the market hit a high not seen since 1998.

The National Association of Realtors said sales of existing U.S. homes eased 2.8 percent in January to a 6.56 million unit annual rate, the slowest pace in nearly two years and the fifth monthly decline in a row.

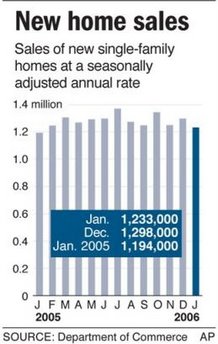

January's sales rate was slightly more sluggish than economists expected. Wall Street had forecast existing home sales at a 6.6 million unit pace. December sales were revised up to a 6.75 million unit annual rate.Chart shows new-home sales for the past 13 months, seasonally adjusted. (AP Graphic)

The existing home sales figure includes both single-family houses and condos.

"The housing market is certainly shifting away from a record-breaking pace," said Lawrence Yun, senior economist for the Realtors.

The figures were the just the latest in a string of data pointing to a cooling in the U.S. housing market after a five-year rally that shattered sales and construction records, and sent prices soaring more than 55 percent across the country.

he Realtors data showed January's decline was driven by a 1.5 percent fall in the pace of single-family home sales and a 10.6 percent drop in condo sales.

Inventories climbed in January by 2.4 percent, leaving 2.91 million existing homes available for sale at the end of the month. That equates to 5.3 months' supply at the current sales pace, the highest since August 1998.

Home prices, however, have been more resilient, and economists chalk that up to sellers trying to cash out at the market's highs. For January, Realtors data show the median home price rose 11.6 percent to $211,000 from a year ago.

According to the Realtors, home sales were easing in the priciest markets where an increase in mortgage rates will have the biggest effect on buying power. Sales dropped 10 percent in the Northeast, 7.7 percent in the Midwest and 3.5 percent in the West.

Looking at these three stories, the big question on my mind is, are we heading for a major recession? These statistics are contradictory. The economy grew at a sluggish pace, consumer confidence fell, and yet unemployment remains low at 4.7 percent (And even there, I have to wonder what the rate is for people who have dropped out of the labor market, or have taken part-time jobs, or jobs that are of a lower skill set). And now the red-hot housing market is starting to show signs of deflating. I'd say a good chunk of the U.S. economic growth has been fueled by the refinancing craze, which allowed American homeowners to swap higher interest rate mortgages for lower interest rate mortgages, which allowed them to pocket--or spend--their interest rate savings. Now that economic stimulus is dying out. What is going to keep Americans spending, when they are starting to worry about job prospects? Throw in the high energy and heating costs that will also eat into the consumers pocketbooks, and perhaps continue to lower consumer confidence, and you've got a convoluted mess here.

I'm looking at these numbers here, and I'm worried. They don't make much sense.

No comments:

Post a Comment