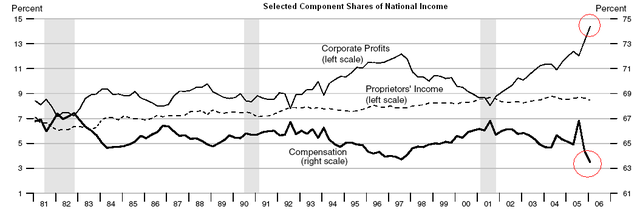

Graphic on Real Wage gains. From New York Times

Graphic on Real Wage gains. From New York TimesThis is off the

New York Times:With the economy beginning to slow, the current expansion has a chance to become the first sustained period of economic growth since World War II that fails to offer a prolonged increase in real wages for most workers.

The median hourly wage for American workers has declined 2 percent since 2003, after factoring in inflation. The drop has been especially notable, economists say, because productivity--the amount that an average worker produces in an hour and the basic wellspring of a nation's living standards--has risen steadily over the same period.

As a result, wages and salaries now make up the lowest share of the nationÂ’s gross domestic product since the government began recording the data in 1947, while corporate profits have climbed to their highest share since the 1960's. UBS, the investment bank, recently described the current period as "the golden era of profitability."

Until the last year, stagnating wages were somewhat offset by the rising value of benefits, especially health insurance, which caused overall compensation for most Americans to continue increasing. Since last summer, however, the value of workers' benefits has also failed to keep pace with inflation, according to government data.

At the very top of the income spectrum, many workers have continued to receive raises that outpace inflation, and the gains have been large enough to keep average income and consumer spending rising.

Think about this for a moment. The stagnating wages have been offset by the rising value of benefits, such as health insurance. But the problem with health insurance is that the price of health insurance has also been increasing, thus adding to companies labor costs. Instead of absorbing the costs of health insurance, companies have started passing those costs towards the workers in terms of higher health insurance premiums deducted from workers' paychecks. At the same time, wage increases have certainly gone to the top income brackets--including those of the CEOs. Thus, the inequality gap between the rich and poor has continued to increase. It is interesting how UBS investment bank has called this period as the “the golden era of profitability," and how corporate profits have climbed to their highest share since the 1960s.

Lyndon Johnson had started both his

Great Society program, and entered into the

Vietnam War. And even Johnson's Great Society economic stimulus was added to

John Kennedy's New Frontier's stimulus, which included tax cuts, economic reforms, wage, housing and medical regulations. There was a lot of economic stimulus in the 1960s, with Americans happily spending on consumer goods, and companies happily producing those consumer goods for profits. The danger of the 1960s economy was that the U.S. government was funding both this economic expansion and the Vietnam War by printing dollar bills--and not by raising taxes to pay for everything. We see the same thing happening now with Bush's tax cut stimulus and war in Iraq. And the economic benefits of globalization and productivity today have been going towards corporate profits, rather than wage increases.

What happens when wages don't increase with inflation? For one thing, consumers are going to feel like they are not getting ahead. The more of their paychecks they spend on rising health insurance premiums, or even increase energy costs, such as high gas prices, the less the consumers are going to spend on all other items. Consumers may just start reducing their spending in the U.S. economy. This will certainly cause business sales to drop, forcing business inventories to increase. Businesses will cut back on their own production, possibly laying off workers and thus exasperating the recession.

Durable goods orders have dropped 2.4 percent--the first decline in durable goods orders in three months. Are businesses starting to cut back? We've already seen

a drop in the housing market. In fact,

sales of new homes have dropped by 4.3 percent in July, resulting in an all-time high inventory of unsold new homes at 568,000. With the sales of U.S. homes dropping, you can also bet that consumers will not be spending money to furnish their homes, thus sales could start dropping on appliances, furniture, and home furnishings.

Chain store sales have dropped 0.2 percent in the week ending August 19. Compared to the same week a year ago, sales rose by 2.7 percent. Is this just a break in consumer spending, or is this the start of a trend with consumers cutting back on spending? I can't say yet. However,

the August 18th consumer sentiment report shows consumer sentiment dropping from 84.7 to 78.7. Wall Street economists were expecting a reading of 83.6. Consumers may be getting pessimistic here. Finally, there is one strange statistic that I do want to toss out here. And that is that the number of first-time jobless claims has dropped by 1,000--from 314,000 to 313,000. I don't know if that is because workers are actually finding jobs, or if they have exhausted their unemployment benefits and are being dropped from the rolls.

What do all these statistics mean? I fear that we may be entering, or are already in, a serious recession. The statistics are showing a slowing economy--that much is certain.

Investors are certainly getting pessimistic here. The real danger we have for this economy is the combination of high energy prices (Which have also been exasperated by the U.S. war in Iraq), and the huge U.S. budget deficit and $8 trillion dollar debt (of which the Bush tax cuts and Iraq war have also contributed to). The budget deficit and debt will certainly cause long term interest rates to remain high. The high energy prices and Iraq war could cause a spike in inflation. There is just too much uncertainty here. Interestingly enough,

the central bankers and Federal Reserve are divided on where the U.S. economy is heading. Consider this:

JACKSON HOLE, Wyoming (Reuters) - Central bankers and top academics departed here on Sunday after two days of discussions on how the global economic landscape is shifting.

But they said goodbye still divided on what is perhaps the biggest question hanging over the outlook -- whether an unfolding slowdown in the U.S. economy will curb U.S. inflation without further interest-rate rises from the Federal Reserve.

"I think this is a time of a fair amount of uncertainty, because certainly there seems to be a shifting in the United States," IMF chief economist Raghuram Rajan said. "We're not quite sure if inflationary pressures are contained ... and we are also not sure how far and how quickly housing will slow."

After two years of steadily pushing benchmark borrowing costs higher, the U.S. central bank stepped to the sidelines at its last meeting on August 8, preferring to wait for more data shedding light on the outlook for growth and inflation.

A downturn in the U.S. housing market is seen cutting the wherewithal of U.S. consumers, who have been able to tap the equity fast rising home prices had provided to maintain their free-spending ways.

Former Brazilian central bank chief Arminio Fraga fretted that a slowdown in the United States, for years an engine supporting growth around the globe, could exact a big toll on economies elsewhere.

"Can the world make up for what is likely to be a slowdown in (U.S.) growth, maybe even a bigger slowdown than one expects at this point -- certainly a deeper slowdown than markets are pricing in?" Fraga asked conference participants.

So both IMF chief economist Rajan and former Brazilian central bank chief Fraga are worried that the high borrowing costs, and the slowing U.S. economic growth is going to cause major problems within the world. That is not surprising, considering that much of the world exports products to the U.S. consumer. If the U.S. consumer cuts back spending on imported goods, then foreign companies will have a backlog of inventory. Do you expect the Third World market to take up the slack for cheap Chinese goods that were once destined for the American consumer? I would also wonder how much knowledge and experience both Rajan and Fraga have had in dealing with Third World countries facing stagflation, high debt levels, dropping wages, rising poverty, inequalities between rich and poor, and stagnating economic growth. Is the United States heading down that path?

I also found

this Yahoo article of conflicting signals from Fed speakers:BLOOMINGTON, Illinois (Reuters) - Two veteran Federal Reserve officials gave different readings on the likely course of interest rate policy on Tuesday -- but only one will be around after the next meeting to implement those views.

Chicago Federal Reserve Bank President Michael Moskow said unequivocally that inflation remains a bigger threat to the U.S. economy than slowing growth, and the central bank might need to raise interest rates again.

By contrast, the soon-to-retire Atlanta Fed Bank President Jack Guynn said U.S. monetary policy was "properly calibrated" and expressed confidence that inflation was going to slow, as the Fed's own forecasts have predicted.

"I am personally comfortably with the notion that policy seems to be properly calibrated," Guynn told reporters after addressing the Kiwanis Club of Atlanta in what could be his final speech as a Fed policy-maker.

Guynn, a Federal Open Market Committee voting member this year, has announced plans to retire October 1 from the Atlanta Fed, which he has led since January 1996.

Not so fast, Moskow said.

In a speech to the McLean County Chamber of Commerce, Moskow said more increases could be needed to trim inflation, which continues to run well above the informal "comfort zone" cited by Moskow and several other Fed policy-makers.

"The risk of inflation remaining too high is greater than the risk of growth being too low. Thus, some additional firming of policy may yet be necessary to bring inflation back into the comfort zone within a reasonable period of time," Moskow said.

There is such irony in this article. First Moskow is worried about the threat of inflation, and the possibility of the Fed raising interest rates. More Fed interest rate increases will be needed to trim inflation. What is especially interesting here is that Moskow is more worried about the rapid rise of inflation, rather than the slowing U.S. economic growth. Moskow doesn't say anything about the risks of stagflation--the increase of inflation along with the slowing U.S. economic growth or recession. But what does Moskow's Federal Reserve compadre Jack Guynn say about inflation and the U.S. economy? Why, things are going swimmingly! "I am personally comfortably with the notion that policy seems to be properly calibrated," is Jack Guynn's statement to the Kiwanis Club of Atlanta. The Feds have done the right job and inflation will slow down, as Guynn is predicting here. Of course, Guynn is also retiring from the Atlanta Fed, so he would want to have this "properly calibrated" economically predicted feather stuck in his career cap. When you've got two Federal Reserve Board members making contradictory statements to the public as to the threat of inflation in the U.S. economy, you've got some serious uncertainty and trouble here.